Page 32 - Contributed Paper Session (CPS) - Volume 1

P. 32

CPS658 Sagaren P.

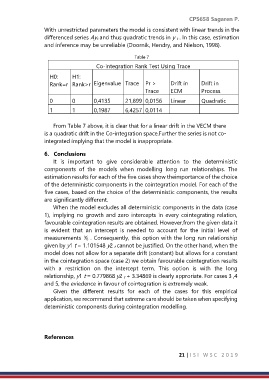

With unrestricted parameters the model is consistent with linear trends in the

differenced series Ayt and thus quadratic trends in y t . In this case, estimation

and inference may be unreliable (Doornik, Hendry, and Nielson, 1998).

Table 7

Co-integration Rank Test Using Trace

H0: H1:

Rank=r Rank>r Eigenvalue Trace Pr > Drift in Drift in

Trace ECM Process

0 0 0,4135 21,899 0,0156 Linear Quadratic

1 1 0,1987 0

6,4257 0,0114

From Table 7 above, it is clear that for a linear drift in the VECM there

is a quadratic drift in the Co-integration space.Further the series is not co-

integrated implying that the model is inappropriate.

6. Conclusions

It is important to give considerable attention to the deterministic

components of the models when modelling long run relationships. The

estimation results for each of the five cases show theimportance of the choice

of the deterministic components in the cointegration model. For each of the

five cases, based on the choice of the deterministic components, the results

are significantly different.

When the model excludes all deterministic components in the data (case

1), implying no growth and zero intercepts in every cointegrating relation,

favourable cointegration results are obtained. However,from the given data it

is evident that an intercept is needed to account for the initial level of

measurements Y0 . Consequently, this option with the long run relationship

given by y1 t = 1.101548 y2 t cannot be justified. On the other hand, when the

model does not allow for a separate drift (constant) but allows for a constant

in the cointegration space (case 2) we obtain favourable cointegration results

with a restriction on the intercept term. This option is with the long

relationship, y1 t = 0.779868 y2 t + 3.34869 is clearly approriate. For cases 3 ,4

and 5, the eviedence in favour of cointegration is extremely weak.

Given the different results for each of the cases for this empirical

application, we recommend that extreme care should be taken when specifying

deteministic components during cointegration modelling.

References

21 | I S I W S C 2 0 1 9