Page 120 - Invited Paper Session (IPS) - Volume 1

P. 120

IPS102 Ilja K. K. et al.

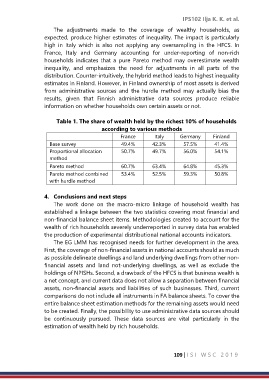

The adjustments made to the coverage of wealthy households, as

expected, produce higher estimates of inequality. The impact is particularly

high in Italy which is also not applying any oversampling in the HFCS. In

France, Italy and Germany accounting for under-reporting of non-rich

households indicates that a pure Pareto method may overestimate wealth

inequality, and emphasizes the need for adjustments in all parts of the

distribution. Counter-intuitively, the hybrid method leads to highest inequality

estimates in Finland. However, in Finland ownership of most assets is derived

from administrative sources and the hurdle method may actually bias the

results, given that Finnish administrative data sources produce reliable

information on whether households own certain assets or not.

Table 1. The share of wealth held by the richest 10% of households

according to various methods

France Italy Germany Finland

Base survey 49.4% 42.3% 57.5% 41.4%

Proportional allocation 50.7% 49.7% 56.0% 54.1%

method

Pareto method 60.7% 63.4% 64.8% 45.3%

Pareto method combined 53.4% 52.5% 59.3% 50.8%

with hurdle method

4. Conclusions and next steps

The work done on the macro-micro linkage of household wealth has

established a linkage between the two statistics covering most financial and

non-financial balance sheet items. Methodologies created to account for the

wealth of rich households severely underreported in survey data has enabled

the production of experimental distributional national accounts indicators.

The EG LMM has recognised needs for further development in the area.

First, the coverage of non-financial assets in national accounts should as much

as possible delineate dwellings and land underlying dwellings from other non-

financial assets and land not-underlying dwellings, as well as exclude the

holdings of NPISHs. Second, a drawback of the HFCS is that business wealth is

a net concept, and current data does not allow a separation between financial

assets, non-financial assets and liabilities of such businesses. Third, current

comparisons do not include all instruments in FA balance sheets. To cover the

entire balance sheet estimation methods for the remaining assets would need

to be created. Finally, the possibility to use administrative data sources should

be continuously pursued. These data sources are vital particularly in the

estimation of wealth held by rich households.

109 | I S I W S C 2 0 1 9