Page 222 - Contributed Paper Session (CPS) - Volume 8

P. 222

CPS2256 Norzarita Samsudin

variable) in the VAR when a shock is applied to the error term. Variance

Decomposition technique separates the variation in the endogenous variable

into the component shocks to the VAR. Thus, the variance decomposition

provides information about the relative importance of each random shock in

affecting the variables in VAR (Ogungbenle, Olawumi and Obasuyi, 2013).

4. Discussion and Conclusion

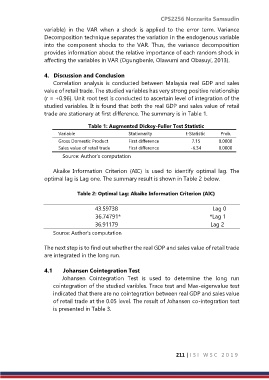

Correlation analysis is conducted between Malaysia real GDP and sales

value of retail trade. The studied variables has very strong positive relationship

(r = +0.96). Unit root test is conducted to ascertain level of integration of the

studied variables. It is found that both the real GDP and sales value of retail

trade are stationary at first difference. The summary is in Table 1.

Table 1: Augmented Dickey-Fuller Test Statistic

Variable Stationarity t-Statistic Prob.

Gross Domestic Product First difference 7.15 0.0000

Sales value of retail trade First difference -6.34 0.0000

Source: Author’s computation

Akaike Information Criterion (AIC) is used to identify optimal lag. The

optimal lag is Lag one. The summary result is shown in Table 2 below.

Table 2: Optimal Lag: Akaike Information Criterion (AIC)

43.59738 Lag 0

36.74791* *Lag 1

36.91179 Lag 2

Source: Author’s computation

The next step is to find out whether the real GDP and sales value of retail trade

are integrated in the long run.

4.1 Johansen Cointegration Test

Johansen Cointegration Test is used to determine the long run

cointegration of the studied varibles. Trace test and Max-eigenvalue test

indicated that there are no cointegration between real GDP and sales value

of retail trade at the 0.05 level. The result of Johansen co-integration test

is presented in Table 3.

211 | I S I W S C 2 0 1 9