Page 361 - Contributed Paper Session (CPS) - Volume 6

P. 361

CPS1966 Jessa L. S. C. et al.

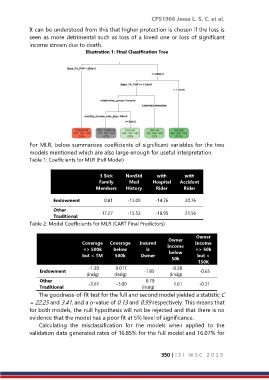

It can be understood from this that higher protection is chosen if the loss is

seen as more detrimental such as loss of a loved one or loss of significant

income stream due to death.

Illustration 1: Final Classification Tree

For MLR, below summarizes coefficients of significant variables for the two

models mentioned which are also large enough for useful interpretation.

Table 1: Coefficients for MLR (Full Model)

3 Sick NonStd with with

Family Med Hospital Accident

Members History Rider Rider

Endowment 0.81 -12.09 -14.76 20.76

Other -17.27 -15.53 -18.95 21.56

Traditional

Table 2: Model Coefficients for MLR (CART Final Predictors)

Owner Owner

Coverage Coverage Insured Income Income

=> 500k below is => 50k

but < 1M 500k Owner below but <

50k

150K

-1.30 0.017 -0.38

Endowment -1.85 -0.65

(insig) (insig) (insig)

Other -3.61 -3.00 0.79 1.61 -0.31

Traditional (insig)

The goodness-of-fit test for the full and second model yielded a statistic C

= 22.25 and 3.41, and a p-value of 0.13 and 0.99 respectively. This means that

for both models, the null hypothesis will not be rejected and that there is no

evidence that the model has a poor fit at 5% level of significance.

Calculating the misclassification for the models when applied to the

validation data generated rates of 16.85% for the full model and 16.07% for

350 | I S I W S C 2 0 1 9