Page 271 - Invited Paper Session (IPS) - Volume 1

P. 271

IPS152 Giovanna B. et al.

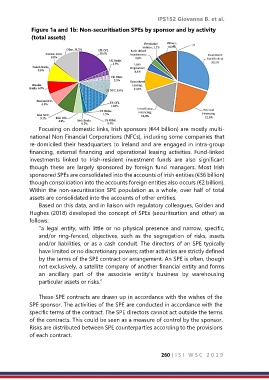

Figure 1a and 1b: Non-securitisation SPEs by sponsor and by activity

(total assets)

Focusing on domestic links, Irish sponsors (€44 billion) are mostly multi-

national Non Financial Corporations (NFCs), including some companies that

re-domiciled their headquarters to Ireland and are engaged in intra-group

financing, external financing and operational leasing activities. Fund-linked

investments linked to Irish-resident investment funds are also significant

though these are largely sponsored by foreign fund managers. Most Irish

sponsored SPEs are consolidated into the accounts of Irish entities (€36 billion)

though consolidation into the accounts foreign entities also occurs (€2 billion).

Within the non-securitisation SPE population as a whole, over half of total

assets are consolidated into the accounts of other entities.

Based on this data, and in liaison with regulatory colleagues, Golden and

Hughes (2018) developed the concept of SPEs (securitisation and other) as

follows:

“a legal entity, with little or no physical presence and narrow, specific,

and/or ring-fenced, objectives, such as the segregation of risks, assets

and/or liabilities, or as a cash conduit. The directors of an SPE typically

have limited or no discretionary powers; rather activities are strictly defined

by the terms of the SPE contract or arrangement. An SPE is often, though

not exclusively, a satellite company of another financial entity and forms

an ancillary part of the associate entity’s business by warehousing

particular assets or risks.”

These SPE contracts are drawn up in accordance with the wishes of the

SPE sponsor. The activities of the SPE are conducted in accordance with the

specific terms of the contract. The SPE directors cannot act outside the terms

of the contracts. This could be seen as a measure of control by the sponsor.

Risks are distributed between SPE counterparties according to the provisions

of each contract.

260 | I S I W S C 2 0 1 9