Page 164 - Special Topic Session (STS) - Volume 4

P. 164

STS577 Md. Sabiruzzaman et al.

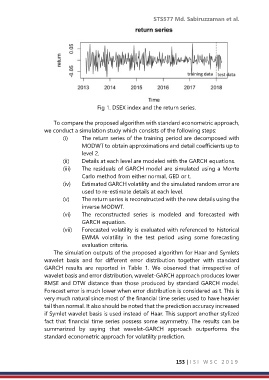

Fig 1. DSEX index and the return series.

To compare the proposed algorithm with standard econometric approach,

we conduct a simulation study which consists of the following steps:

(i) The return series of the training period are decomposed with

MODWT to obtain approximations and detail coefficients up to

level 2.

(ii) Details at each level are modeled with the GARCH equations.

(iii) The residuals of GARCH model are simulated using a Monte

Carlo method from either normal, GED or t.

(iv) Estimated GARCH volatility and the simulated random error are

used to re-estimate details at each level.

(v) The return series is reconstructed with the new details using the

inverse MODWT.

(vi) The reconstructed series is modeled and forecasted with

GARCH equation.

(vii) Forecasted volatility is evaluated with referenced to historical

EWMA volatility in the test period using some forecasting

evaluation criteria.

The simulation outputs of the proposed algorithm for Haar and Symlets

wavelet basis and for different error distribution together with standard

GARCH results are reported in Table 1. We observed that irrespective of

wavelet basis and error distribution, wavelet-GARCH approach produces lower

RMSE and DTW distance than those produced by standard GARCH model.

Forecast error is much lower when error distribution is considered as t. This is

very much natural since most of the financial time series used to have heavier

tail than normal. It also should be noted that the prediction accuracy increased

if Symlet wavelet basis is used instead of Haar. This support another stylized

fact that financial time series possess some asymmetry. The results can be

summarized by saying that wavelet-GARCH approach outperforms the

standard econometric approach for volatility prediction.

153 | I S I W S C 2 0 1 9