Page 204 - Special Topic Session (STS) - Volume 1

P. 204

STS425 Arifah B. et al.

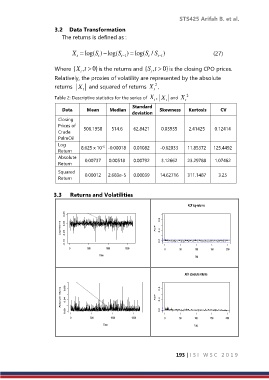

3.2 Data Transformation

The returns is defined as :

X log( ) log(S S t 1 ) log( /S S t t 1 ) (27)

t

t

Where { ,X t 0}is the returns and { ,S t 0}is the closing CPO prices.

t

t

Relatively, the proxies of volatility are represented by the absolute

2

returns X and squared of returns X ,

t

t

Table 2: Descriptive statistics for the series of X t , X t and X t 2

Standard

Data Mean Median Skewness Kurtosis CV

deviation

Closing

Prices of 506.1958 514.6 62.8421 0.03935 2.41425 0.12414

Crude

PalmOil

Log 8.625 x 10 -0.00018 0.01082 -0.62033 11.85372 125.4492

-5

Return

Absolute 0.00737 0.00518 0.00792 3.12662 23.29788 1.07462

Return

Squared 0.00012 2.683e-5 0.00039 14.62716 311.1487 3.25

Return

3.3 Returns and Volatilities

ACF log-returns

0.05

0.8

Log-returns -0.05 ACF 0.4

0.00

-0.10 0.0

0 500 1000 1500 0 50 100 150 200

Time Lag

ACF absolute returns

Absolute returns 0.08 0.04 ACF 0.8 0.4

0.00 0.0

0 500 1000 1500 0 50 100 150 200

Time Lag

193 | I S I W S C 2 0 1 9