Page 279 - Contributed Paper Session (CPS) - Volume 6

P. 279

CPS1929 Takayuki M.

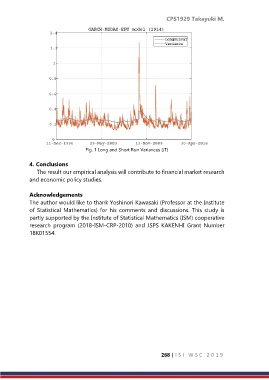

Fig. 1 Long and Short Run Variances (JT)

4. Conclusions

The result our empirical analysis will contribute to financial market research

and economic policy studies.

Acknowledgements

The author would like to thank Yoshinori Kawasaki (Professor at the Institute

of Statistical Mathematics) for his comments and discussions. This study is

partly supported by the Institute of Statistical Mathematics (ISM) cooperative

research program (2018-ISM-CRP-2010) and JSPS KAKENHI Grant Number

18K01554.

268 | I S I W S C 2 0 1 9